The 2017 Tax Cuts and Jobs Act (TCJA) marked a seismic shift in the landscape of American tax policy, sparking intense debates over its ramifications. Enacted with the promise to stimulate economic growth through substantial corporate tax cuts, the TCJA fundamentally altered how corporations would interact with the federal tax framework. As economists and policymakers continue to analyze its impact, findings from studies like the Chodorow-Reich study reveal a nuanced picture of modest wage increases and business investments alongside a staggering decline in federal tax revenue. This ongoing corporate tax debate has given rise to competing perspectives on how best to balance tax cuts with the essential funding of public services. As critical pieces of the TCJA face expiration, the conversation surrounding corporate tax cuts and their long-term consequences remains at the forefront of national discussions.

Introduced amidst a climate of economic transformation, the 2017 Tax Cuts and Jobs Act has brought significant attention to the intricacies of tax legislation. Often referenced as a pivotal moment in corporate finance, this tax reform initiative intended to foster growth by cutting corporate tax rates. The comprehensive tax policy analysis surrounding the TCJA continues to inform discussions about the relationship between taxation and corporate behavior. As diverse studies explore corporate tax cuts’ impact, particularly within the context of rising federal tax revenue and liabilities, experts like Gabriel Chodorow-Reich are reshaping the narrative about corporate tax responsibilities. In light of pending expirations of certain provisions, the examination of this policy’s effectiveness and implications remains crucial for future fiscal strategies.

The Impact of the 2017 Tax Cuts and Jobs Act on Federal Revenue

The 2017 Tax Cuts and Jobs Act (TCJA) marked a significant shift in U.S. tax policy, particularly regarding corporate tax rates. Initially, the enactment of the TCJA resulted in a dramatic decline of about 40% in corporate tax revenue, raising concerns amongst economists and policymakers alike. This drastic fall was anticipated, as the TCJA permanently reduced the corporate tax rate from 35% to 21%. Proponents argued that this would stimulate the economy through increased investments and growth, leading to a larger tax base; however, the immediate aftermath painted a stark picture of declining revenue.

As the years progressed, the narrative surrounding federal revenue began to shift. By 2020, corporate tax revenues rebounded, rising beyond what many analysts had expected. This resurgence can be attributed to a combination of factors, including unexpected corporate profits and a simplified global tax landscape post-TCJA. The preceding years of economic expansion had also allowed companies to accumulate more capital, prompting them to channel a portion of their profits back into the U.S., thus benefitting federal tax revenues. The dynamic nature of corporate taxes illustrates the complexity of tax policy analysis, making it clear that while the TCJA initially detracted from revenue, it also set the stage for later gains.

Corporate Tax Debate: Balancing Cuts and Rates

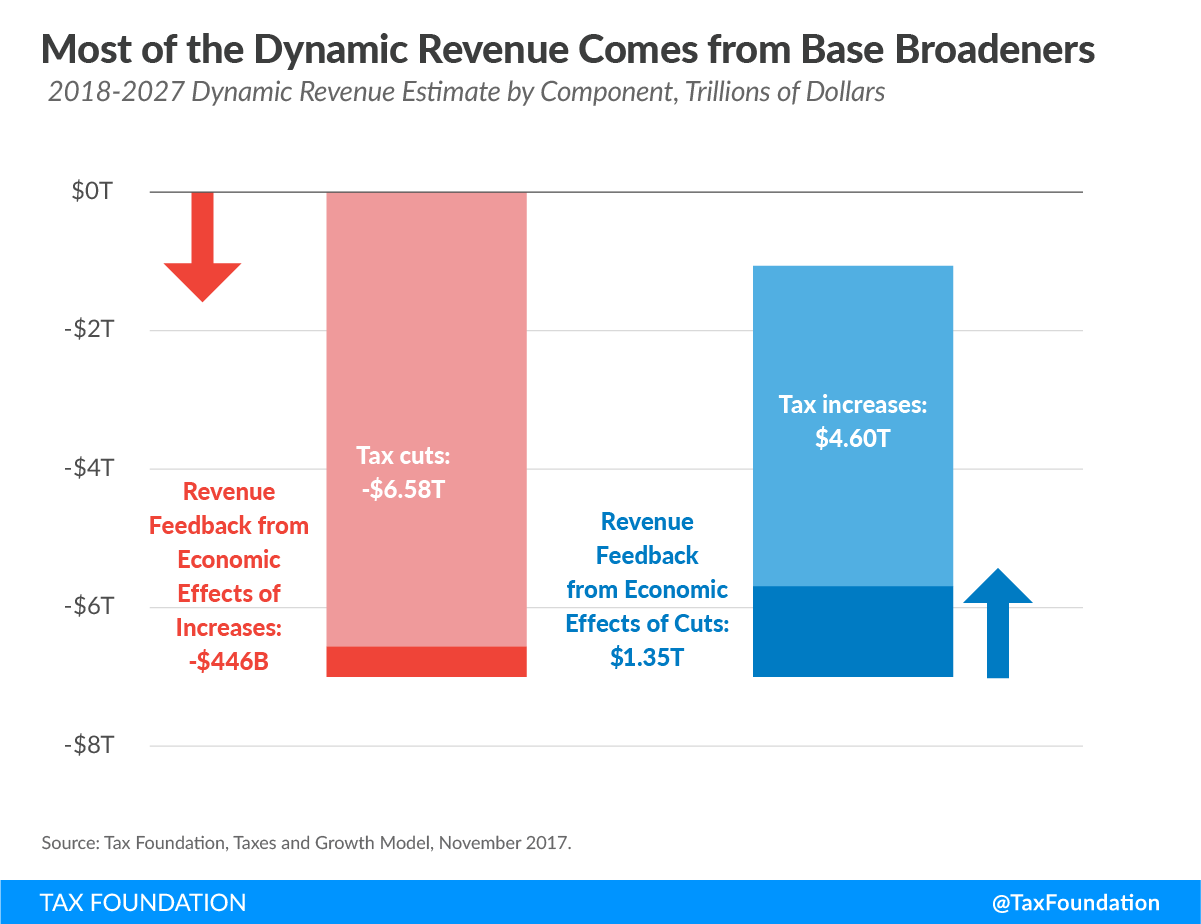

The corporate tax debate has intensified in light of the TCJA, with Republicans and Democrats presenting starkly opposing views on the best path forward. Advocates for higher corporate tax rates argue that increasing these rates can provide the necessary funding for crucial public services and initiatives, such as education and healthcare. This perspective aligns with findings from studies like the Chodorow-Reich study, which highlight a nuanced understanding of corporate tax cuts’ impact—specifically that they may not lead to the expansive economic benefits originally promised. Consequently, raising rates could encourage a more balanced approach to tax policy that sustains revenue while fostering investment.

On the flip side, opponents of tax increases, particularly those from the Republican camp, maintain that further cuts are essential to incentivize growth and innovation. They argue that lower corporate tax rates attract businesses to the U.S. and stimulate job creation. This contention often relies on the belief that historical data supports substantial gains in investment due to reduced tax liability. As the 2025 tax battleground looms, these divergent views highlight the significance of corporate tax cuts in shaping economic outcomes and federal policy, emphasizing the need for a careful analysis of the implications surrounding any changes in the current tax structure.

Insights from the Chodorow-Reich Study

The Chodorow-Reich study provides specific insights into the consequences of the TCJA on business investment and wage growth. Co-authored by Gabriel Chodorow-Reich, the research examines the direct effects of corporate tax cuts on capital investments, revealing an approximate increase of 11% in such spending post-TCJA. This increase signals that corporations indeed respond to tax policy changes, which contradicts some longstanding assertions that taxes have negligible effects on corporate behavior. It further informs the corporate tax debate by delineating the effectiveness of expensing measures over mere rate cuts in driving meaningful economic activity.

However, one of the study’s most critical findings is the modest connection between corporate tax adjustments and wage growth. While the Council of Economic Advisers projected significant wage increases following the TCJA, the actual figures reported by Chodorow-Reich and his co-authors were significantly lower—around $750 per year in 2017 dollars. This discrepancy illustrates the complexity of the corporate tax debate, as it challenges the notion that cuts automatically translate into enhanced worker compensation, thereby fostering a need for more comprehensive and nuanced tax policy analysis.

The Sunsetting Provisions of the TCJA

As the TCJA provisions near expiration at the end of 2025, the conversation around what should be renewed or repealed is heating up. Among the most contentious issues is the fate of the corporate tax cuts versus the incentives designed for families, such as the enhanced Child Tax Credit. With many voters anxious about the ratification of these provisions, lawmakers are caught in a tug-of-war over priorities—whether to prioritize corporate benefits that ostensibly stimulate economic growth or maintain incentives aimed at lower and middle-income households.

The sunsetting provisions could offer an opportunity to reassess the corporate tax cuts’ actual economic impact. Politicians and economists alike are scrutinizing the effectiveness of these provisions in fostering substantial investments and job creation. As Congress prepares for debate, stakeholders will need to consider not just the fiscal implications but also how different tax policies align with broader economic goals—ensuring the maximization of federal tax revenue while supporting households and businesses alike.

Bipartisan Recognition of Tax Reform Needs

There was bipartisan awareness that reform was essential by the time the TCJA was enacted in late 2017. Economists and political leaders from both parties acknowledged that the U.S. corporate tax structure was lagging behind other developed nations, with the statutory rate being one of the highest globally at that time. This recognition spurred the urgency to implement reforms that would address not only the rate itself but also the complexity of the corporate tax code, which had not seen significant updates in over 30 years.

This bipartisan agreement reflects broader trends within tax policy analysis, as both parties recognized the potential of tax reform to stimulate the economy in a rapidly changing global landscape. The need for tax cuts targeted at corporations was seen as a strategy to combat international tax competition—encouraging domestic investment and retaining businesses. However, moving forward, a balanced dialogue that includes considerations for revenue generation, tax equity, and corporate accountability will be essential to ensure that any forthcoming reforms genuinely address the diverse economic challenges facing the U.S.

Evaluating Tax Cuts versus Investment Incentives

A pivotal aspect of the ongoing corporate tax debate centers on the effectiveness of tax cuts compared to targeted investment incentives. The TCJA’s provisions allowed companies to write off investments more quickly, a strategy that was arguably more successful in stimulating capital spending than traditional rate cuts on their own. Chodorow-Reich’s findings highlight the unintended consequences of solely relying on corporate tax cuts without implementing structured incentives that align more closely with economic growth objectives.

This distinction holds important implications for future tax policies. As lawmakers contemplate increasing corporate tax rates, there’s an opportunity to restore targeted tax incentives that have proven to yield higher returns in stimulating business investment. The notion of optimizing corporate tax policy through a combination of rate adjustments and strategic incentives could foster an economic environment that bolsters business growth while enhancing federal revenues, which is paramount in light of budgetary challenges.

The Future of Corporate Taxation and Economic Growth

Looking ahead, the future of corporate taxation will play a crucial role in either reinforcing or undermining economic growth in the U.S. If Congress opts to raise corporate tax rates in 2025, the decision must balance the need for immediate fiscal health against the long-term vision for sustainable growth. While increased rates could result in enhanced federal revenues to fund essential services and public investment, they must not disincentivize the capital formation that fuels economic expansion.

Ultimately, the challenge lies in crafting a corporate tax policy that effectively promotes investments while ensuring equitable tax contributions from businesses. Evaluating the historical performance of the TCJA—especially insights from studies like the Chodorow-Reich analysis—can enhance the understanding of the relationship between corporate taxes and economic indicators, thus guiding policymakers in navigating this complex terrain effectively.

Corporate Responsibility and Tax Policy

In the context of increasing scrutiny on corporate behavior, tax policy must also consider the notion of corporate responsibility. The TCJA’s cuts were initially heralded as a way to boost growth, yet the subsequent events raised questions about how corporations utilize their tax savings. Are these funds being reinvested into the workforce or returned to shareholders? Understanding these dynamics has become crucial in shaping tax policy that aligns with societal expectations around corporate accountability.

As discussions about raising corporate tax rates gain traction, there lies the opportunity to foster a tax policy that incentivizes responsible corporate behavior. Encouraging firms to reinvest in their workforce and sustainable practices can be a win-win—helping to boost economic growth while ensuring that corporations contribute fairly to the society that enables their success. Thus, developing a responsible corporate tax regime will be central to future debates, particularly with the lessons learned from the TCJA in mind.

Long-term Economic Implications of Corporate Tax Cuts

The long-term economic implications of the corporate tax cuts from the TCJA are still manifesting as various sectors assess the outcome of these policies. While immediate impacts included a sharp decline in federal tax revenue, subsequent years suggested a more complex picture where growth in corporate profits outpaced initial revenue losses. This paradox has led economists and policymakers to revisit assumptions about fiscal responsibility and the efficacy of tax reductions as an economic strategy.

Furthermore, analyzing the lasting impacts of the corporate tax cuts requires scrutinizing not just revenue generation, but also measuring the overall health of the economy, including job creation and wage growth. These elements signify the broader ramifications of tax policy and emphasize the importance of a balanced approach that weighs both short-term fiscal considerations against long-term economic objectives. A comprehensive evaluation of the TCJA outcomes will be essential as legislators prepare for the upcoming tax policy discussions in 2025.

Frequently Asked Questions

What are the key features of the 2017 Tax Cuts and Jobs Act (TCJA)?

The 2017 Tax Cuts and Jobs Act (TCJA) included significant provisions such as lowering the corporate tax rate from 35% to 21%, allowing immediate expensing of capital investments, and changes to personal income tax brackets. These measures were intended to stimulate economic growth and investment while addressing previous competitive disadvantages in the global market.

How did the corporate tax cuts in the 2017 Tax Cuts and Jobs Act affect federal tax revenue?

The corporate tax cuts implemented by the 2017 Tax Cuts and Jobs Act initially caused a 40% drop in federal corporate tax revenue. However, by 2020, corporate tax revenues began to recover and even surpass expectations, largely due to an unexpected surge in business profits during the pandemic.

What findings did the Chodorow-Reich study reveal about the impact of the 2017 Tax Cuts and Jobs Act on business investments?

The Chodorow-Reich study indicated that the corporate tax cuts from the 2017 Tax Cuts and Jobs Act resulted in an approximate 11% increase in capital investments. It highlighted that provisions for immediate expensing drove this growth more effectively than traditional statutory rate cuts.

Was there a direct correlation between the 2017 Tax Cuts and Jobs Act and wage increases?

While the 2017 Tax Cuts and Jobs Act was expected to boost wages, the actual increase was modest, estimated at about $750 per year per full-time employee, rather than the predicted $4,000 to $9,000. This suggests that while there was some impact, it fell short of the initial expectations set by proponents of the TCJA.

Are there ongoing debates about raising corporate tax rates following the 2017 Tax Cuts and Jobs Act?

Yes, there is an ongoing debate regarding whether to raise corporate tax rates in light of the findings from studies like Chodorow-Reich’s analysis. As some provisions of the TCJA are set to expire, discussions about balancing corporate tax rates with investment incentives continue to be a significant aspect of tax policy analysis.

How have the corporate tax cuts under the 2017 Tax Cuts and Jobs Act influenced political discourse?

The corporate tax cuts under the 2017 Tax Cuts and Jobs Act have become a focal point in political campaigns, with discussions highlighting the need to either renew these cuts or increase corporate tax rates to finance other social initiatives. This has made corporate tax policy a partisan issue in the lead-up to elections.

What is the long-term outlook for the provisions of the 2017 Tax Cuts and Jobs Act?

The long-term outlook for the provisions of the 2017 Tax Cuts and Jobs Act remains uncertain, as many tax cuts for individuals are set to expire after 2025, prompting ongoing debates about their renewal. The impact on corporate tax strategies will continue to be analyzed as lawmakers assess the effectiveness of these tax policies.

How did the 2017 Tax Cuts and Jobs Act affect international competition for corporate taxation?

The 2017 Tax Cuts and Jobs Act was a response to increased international competition in corporate taxation. By reducing the U.S. corporate tax rate, the TCJA aimed to make American corporations more competitive globally, as other countries had been decreasing their corporate taxes to attract business investments.

What role did the 2017 Tax Cuts and Jobs Act play in the broader economic context?

The 2017 Tax Cuts and Jobs Act was crucial in pivoting U.S. tax policy to adapt to a more global economy, addressing the competitive disadvantage faced by U.S. companies. Its provisions aimed at stimulating economic growth, but the overall effectiveness and long-term results are subject to analysis and debate among economists.

What impact did the 2017 Tax Cuts and Jobs Act have on corporate profits?

Following the implementation of the 2017 Tax Cuts and Jobs Act, corporate profits soared, contributing to unexpected increases in corporate tax revenue starting in 2020, despite an initial decline. Factors such as pandemic-related market dynamics and shifts in global profit reporting contributed to this rise.

| Key Points | Details |

|---|---|

| Impact of 2017 Tax Cuts and Jobs Act (TCJA) | The TCJA, enacted to reform the outdated corporate tax system, permanently reduced corporate tax rates from 35% to 21%. |

| Expiration of Provisions | Key provisions like the expanded Child Tax Credit are set to expire by the end of 2025. |

| Corporate Tax Revenue | Following the TCJA, federal corporate tax revenue dropped 40%, but rebounded and exceeded expectations starting in 2020. |

| Business Investment | Analysis shows capital investments increased by about 11% due to the TCJA, particularly from expensing provisions. |

| Wage Effects | Predicted wage increases post-TCJA were not met; actual annual increases were estimated at approximately $750. |

| Future Tax Debates | With impending expirations and ongoing corporate tax discussions, debates are heating up as elections approach. |

Summary

The 2017 Tax Cuts and Jobs Act (TCJA) aimed to revitalize the U.S. corporate tax landscape by reducing the statutory rate significantly. While the law initially increased capital investments, the anticipated wage growth fell short of expectations. Moreover, with crucial elements like the expanded Child Tax Credit poised to expire soon, the debate surrounding the TCJA is only intensifying as we approach the election year, pressing lawmakers to reconsider corporate tax structures for future economic stability.